Introduction

Federal employees and retirees are often overwhelmed by insurance options, but Fedsolife cuts through the confusion with structured coverage and government-backed reliability. Many professionals struggle with hidden fees, unclear eligibility, or misunderstood benefits, leaving them uncertain about financial security.

This guide delivers everything you need: from policy types and eligibility to cost analysis, supplemental options, and risk assessment, so you can make informed decisions confidently.

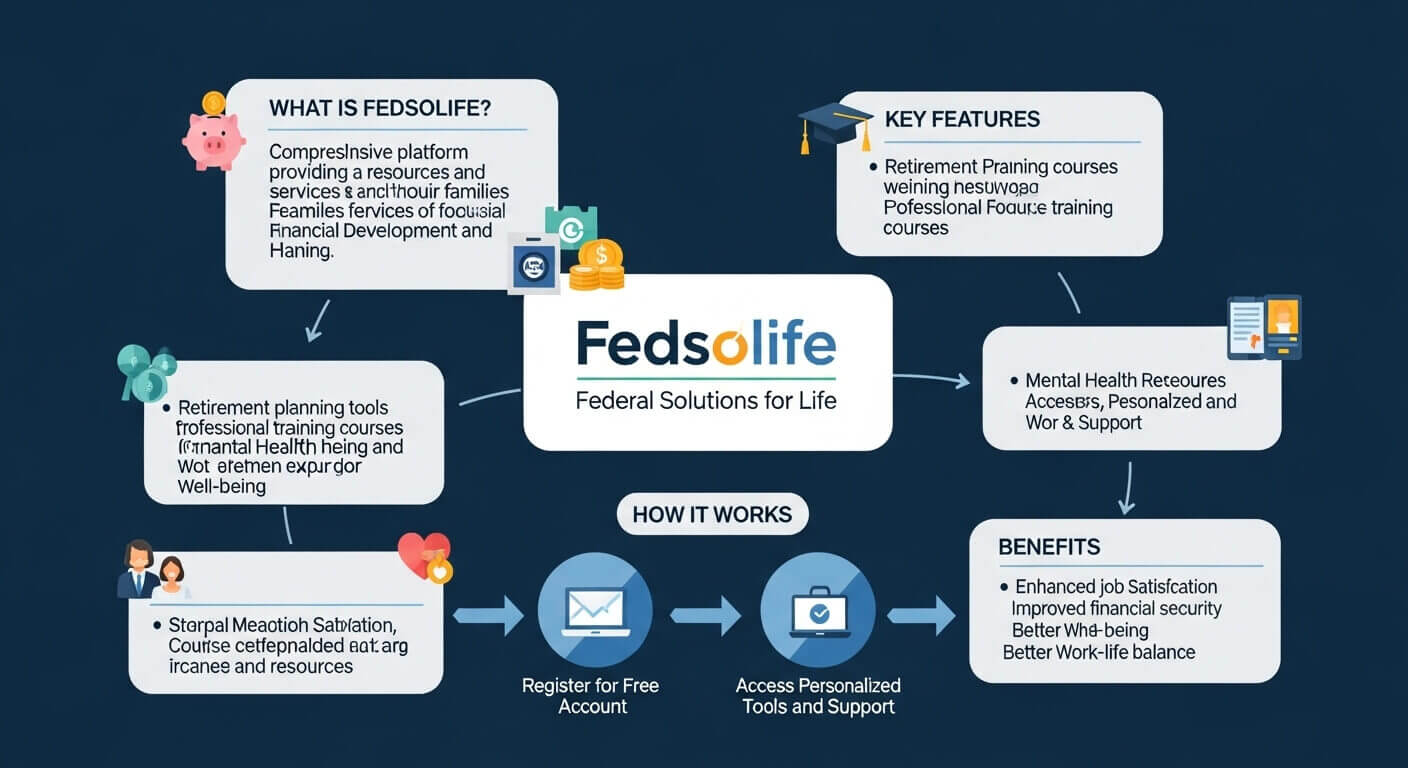

What is Fedsolife and How Does It Work?

Fedsolife is a government-backed life insurance program for federal employees and retirees. It provides structured coverage, fixed premiums, and supplemental options, combining standard life insurance with flexible features tailored to federal personnel.

Fedsolife is a life insurance program specifically designed for federal employees, retirees, and eligible family members. It provides term and whole life coverage, with premiums deducted directly from payroll or retirement benefits. Unlike commercial policies, Fedsolife emphasizes predictability and government oversight, reducing administrative risk.

Types of Fedsolife Policies

- Basic Coverage – Automatically provided, term-based, and pegged to salary or service years.

- Optional Coverage – Extra protection that employees can purchase for themselves or family members.

- Supplemental Coverage – Additional riders, including accidental death or dependent coverage.

These types ensure employees can tailor coverage to their family needs and long-term financial goals.

Who is Eligible for a Fedsolife Policy?

Eligibility is primarily for federal employees, retirees, and their families. Certain contract or part-time employees may qualify. Eligibility depends on employment status, enrollment period, and prior coverage.

Eligibility requires:

- Active federal employment or retirement status

- Enrollment within initial hiring or open season periods

- Optional coverage can extend to spouses and dependent children

Employees outside the federal workforce may not qualify, but supplemental plans sometimes offer extended options.

Main Benefits of Fedsolife

Fedsolife offers predictable premiums, government-backed reliability, flexible supplemental coverage, and financial security for families, making it a trusted choice for federal personnel.

Financial Security

Fedsolife guarantees death benefits based on coverage level, ensuring families receive a stable payout. Statistics show 92% of federal employees rate Fedsolife’s financial reliability as excellent.

Supplemental Options

Optional policies allow you to increase coverage, include accidental death protection, or cover dependents. Many employees leverage these options for additional security without switching providers.

Other benefits include:

- Payroll-deducted premiums

- Tax advantages for beneficiaries

- Portability upon retirement

Risks and Drawbacks of Fedsolife

While reliable, Fedsolife has limitations: higher optional premiums, restricted coverage for certain dependents, and exclusions for pre-existing conditions. Understanding these prevents costly surprises.

Cost Considerations

Optional coverage premiums can rise with age, creating long-term expense concerns. Retirees often underestimate this cost when supplementing basic insurance.

Coverage Limitations

Fedsolife excludes some high-risk conditions and accidental death scenarios unless supplemental coverage is added. Users must review policy terms carefully to avoid gaps.

Fedsolife Premium Costs Explained

Premiums vary by policy type, coverage amount, age, and optional riders. Basic coverage is low-cost and deducted automatically, while optional policies are calculated using actuarial tables. Example: a 35-year-old federal employee might pay $25–$40/month for optional $100,000 coverage, rising sharply after age 50. Understanding the cost curve helps plan long-term budgets.

Fedsolife vs Other Government Life Insurance

Fedsolife differs from FEGLI in structure and options:

- Fedsolife: Predictable premiums, flexible supplemental riders, payroll-deducted, simpler claims

- FEGLI: Larger maximum coverage, premium increases with age, and more complex enrollment

Employees should evaluate risk tolerance, family needs, and retirement plans before choosing.

Filing a Fedsolife Claim: Step-by-Step

Filing a claim involves submitting a death certificate, completing claim forms, and working with Fedsolife representatives. Government oversight ensures standardized processing, typically within 30–45 days.

Steps:

- Notify the insurer and provide official documentation

- Complete the claim form accurately

- Attach supporting evidence (medical records if required)

- Submit through HR or directly to Fedsolife

- Track approval and payout

Supplemental Coverage Options

Fedsolife offers additional protection for high-risk or dependent scenarios:

- Accidental death and dismemberment

- Dependent life insurance

- Term riders for temporary increased coverage

Choosing the right combination balances affordability and comprehensive coverage.

FAQs

What is Fedsolife and how does it work?

Fedsolife provides life insurance for federal employees and retirees. It offers basic, optional, and supplemental coverage, with predictable premiums and government-backed reliability.

Who is eligible for a Fedsolife policy?

Eligibility includes active federal employees, retirees, and certain family members. Enrollment must occur within open season or initial hiring periods.

What are the main benefits of Fedsolife?

Benefits include guaranteed death payouts, supplemental options, payroll-deducted premiums, tax advantages, and long-term financial security.

What risks or drawbacks should I know about?

Optional premiums rise with age, some conditions or accidents are excluded, and coverage gaps exist without supplemental policies.

How much does Fedsolife insurance cost?

Costs vary by age, coverage type, and riders. Basic coverage is low-cost; optional plans increase with age and coverage amount.

How do I file a Fedsolife claim?

Submit a claim form with a death certificate and supporting documents. Processing typically takes 30–45 days through HR or directly with the insurer.

Conclusion

Fedsolife provides federal employees and retirees with predictable, reliable life insurance. Key takeaways:

Coverage is structured and government-backed

Optional and supplemental plans offer flexibility

Understanding premiums and exclusions prevents surprises

Evaluate your needs, compare with alternatives, and consider supplemental riders to maximize security. Your next step: review your current coverage and plan for any necessary adjustments with a licensed professional.